Cannabis Insurance in New York: The Complete Guide for Licensed Operators in 2026

New York’s legal cannabis market is growing fast, but insuring a cannabis business is nothing like insuring a traditional retail store or manufacturing operation. The federal classification of marijuana, the complex state licensing requirements overseen by the Office of Cannabis Management, and the unique operational risks of growing, processing, and selling cannabis create an insurance landscape that most business owners find confusing and frustrating. This guide breaks down the coverage every New York cannabis operator needs, the regulatory requirements you must meet to keep your license, and how to find carriers that actually want to write cannabis policies.

Why Cannabis Insurance Is Different from Traditional Business Insurance

The single biggest factor that makes cannabis insurance unique is the federal and state regulatory disconnect. While New York fully legalized adult-use cannabis, the substance remains federally classified as a controlled substance. This creates a ripple effect across the insurance industry. Many of the largest national carriers will not write policies for cannabis businesses at all because they view the federal legal risk as too high. The carriers that do write cannabis coverage often charge significantly higher premiums than comparable policies for non-cannabis businesses.

Beyond the federal issue, cannabis businesses face operational risks that most traditional businesses do not. Dispensaries handle large amounts of cash because many banks still will not serve cannabis companies. Cultivation facilities use high-intensity lighting, irrigation systems, and chemical nutrients that create fire, water damage, and environmental liability risks. Processing and extraction operations involve flammable solvents and pressurized equipment. And every business in the supply chain faces product liability exposure if a consumer claims harm from a cannabis product.

Insurance Requirements for New York Cannabis License Holders

The New York State Office of Cannabis Management requires licensed operators to demonstrate adequate insurance coverage as part of the licensing and renewal process. While the OCM does not always specify exact coverage limits for every license type, the practical requirements are well established through regulatory guidance, application conditions, and the expectations of landlords, investors, and lenders.

Licensing Requirement: Proof of insurance is a prerequisite for obtaining and maintaining a cannabis license in New York. Many applicants are required to demonstrate adequate liability coverage, and some license types require the OCM to be listed as an additional insured party on your policies.

Cultivators

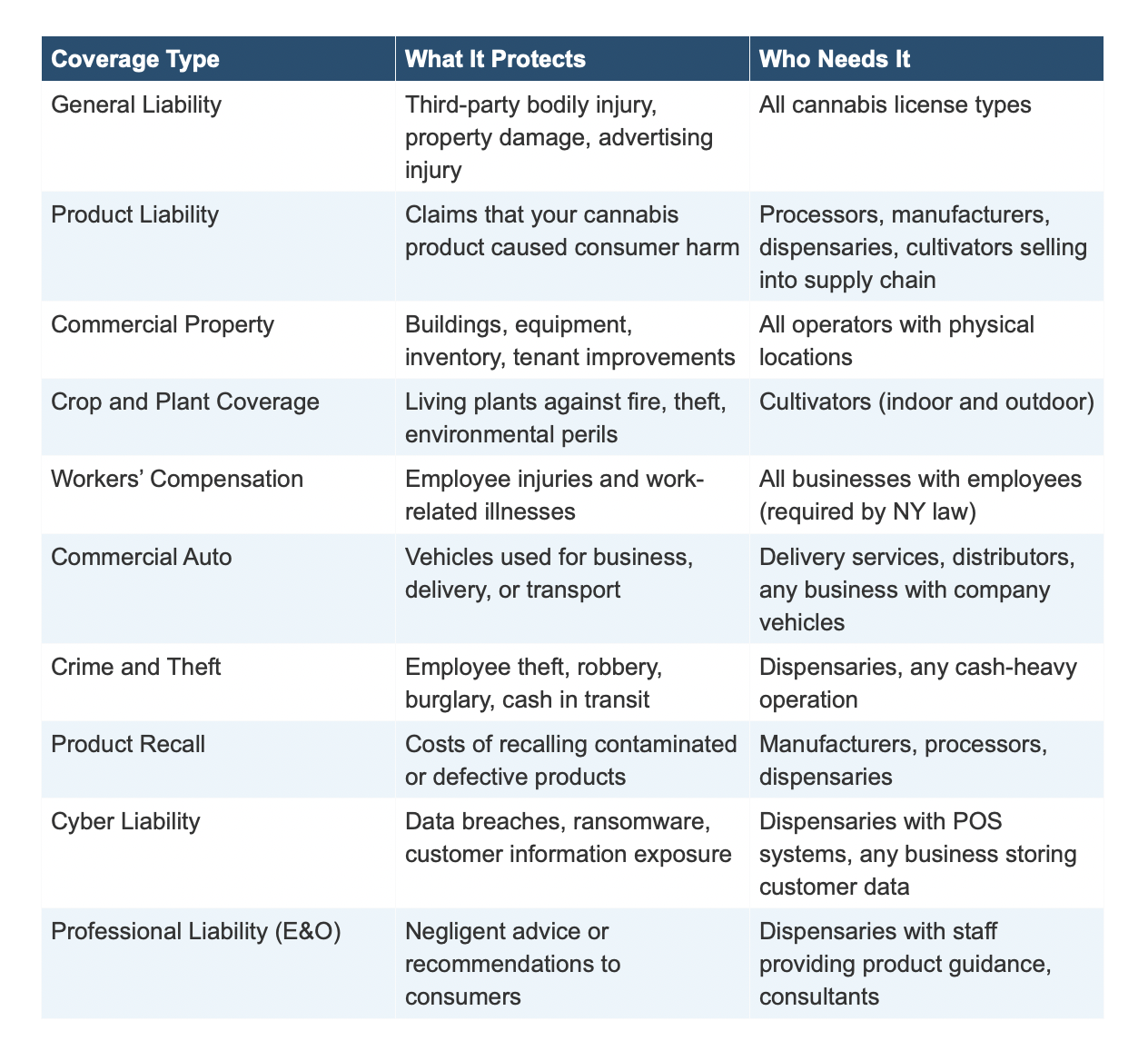

Cannabis cultivation operations face a combination of agricultural, property, and liability risks. Cultivators need general liability insurance to cover premises injuries, property and equipment coverage for grow facilities, lighting rigs, irrigation systems, and processing equipment, and product liability coverage once harvested product enters the supply chain. Crop coverage, where available, can insure living plants against fire, theft, and certain environmental perils, though options remain limited compared to traditional agriculture.

Processors and Manufacturers

Processing and manufacturing operations carry elevated risk due to extraction methods that may involve flammable solvents, CO2 systems, and pressurized equipment. These businesses need robust general liability and product liability policies, along with property coverage that specifically addresses the hazards of extraction and manufacturing processes. Pollution liability may also be necessary depending on the chemicals and waste products involved in your operation.

Dispensaries and Retail Operations

Dispensaries face the most consumer-facing risks in the cannabis supply chain. General liability insurance is essential to cover slip-and-fall injuries and other premises claims. Product liability coverage protects against claims that a product sold at your dispensary caused harm to a consumer. Because dispensaries often handle significant cash on-site, crime and theft insurance is critical. If your dispensary offers delivery services, you will also need commercial auto insurance that meets New York’s minimum financial responsibility requirements.

Distributors and Delivery Services

Businesses that transport cannabis products between licensed facilities or directly to consumers face transit-related risks that require commercial auto coverage, inland marine or cargo insurance for products in transit, and general liability. New York’s delivery regulations add complexity, and your insurance program needs to account for the specific routes, vehicles, and volumes your operation handles.

Essential Coverage Types for Cannabis Businesses

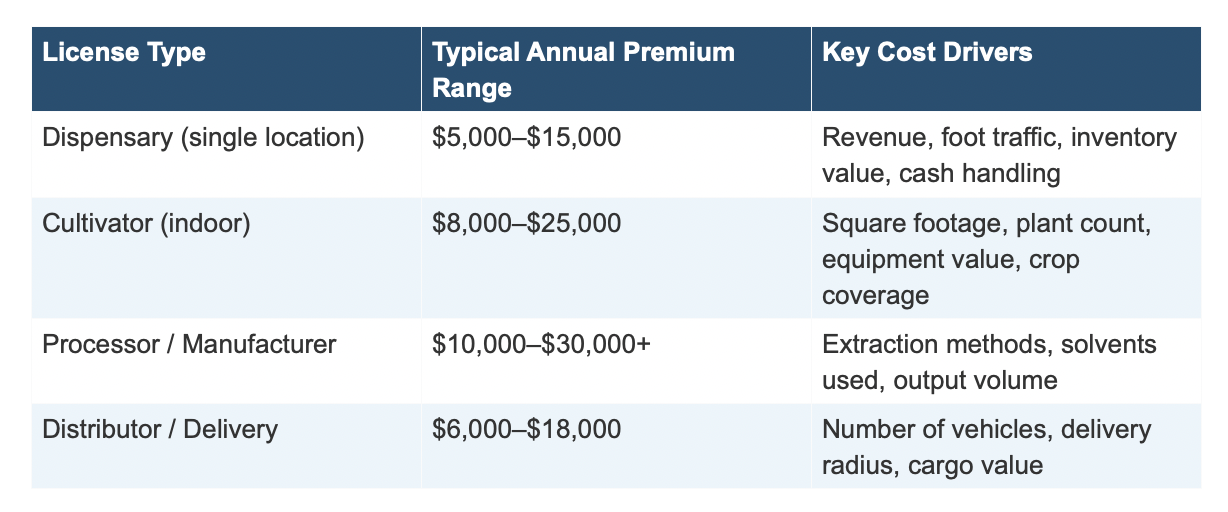

How Much Does Cannabis Insurance Cost in New York?

Cannabis insurance premiums are higher than comparable coverage for non-cannabis businesses, but costs vary widely depending on your license type, revenue, location, number of employees, and claims history. As a general benchmark, a dispensary can expect to pay between $5,000 and $15,000 annually for a comprehensive coverage package that includes general liability, product liability, property, and workers’ compensation. Cultivation and manufacturing operations with higher risk profiles may pay significantly more, particularly if extraction processes involve flammable materials.

License TypeTypical Annual Premium RangeKey Cost Drivers

These ranges are approximate and can shift based on your specific operation, carrier appetite, and market conditions. The cannabis insurance market is still maturing, and new carriers entering the space are beginning to create more competitive pricing for well-run operations with clean claims histories.

The Biggest Insurance Challenges Cannabis Businesses Face

Limited Carrier Availability

The most frustrating challenge for cannabis operators is finding carriers willing to write coverage at all. Because cannabis remains federally classified as a controlled substance, most major national insurance companies will not insure cannabis businesses. This means operators are often limited to specialty carriers and surplus lines insurers, which can mean higher premiums and fewer coverage options. Working with a broker who has established relationships with cannabis-friendly carriers is essential for accessing the best available options.

Coverage Gaps and Exclusions

Even when you find a carrier, the policy language matters enormously. Some general liability policies contain exclusions that effectively void coverage for cannabis-related claims. Property policies may exclude or sub-limit coverage for cannabis inventory. And business interruption coverage, which would pay for lost income if your operation is forced to close temporarily, can be difficult to obtain because valuing cannabis inventory remains a challenge for many insurers.

Banking and Payment Complications

Many cannabis businesses operate primarily in cash because traditional banks are reluctant to serve the industry. This creates elevated theft and robbery risk, complicates payroll and financial record-keeping, and can make it harder to demonstrate financial stability to insurers. Businesses that have secured banking relationships are generally viewed more favorably by carriers and may qualify for better rates.

Evolving Regulations

New York’s cannabis regulatory framework continues to evolve as the Office of Cannabis Management refines its rules and more licenses are issued. Insurance requirements can change with new regulatory guidance, and operators need to stay current to maintain compliance. A broker who actively monitors the regulatory landscape can help you adjust your coverage proactively rather than scrambling to catch up after a requirement changes.

Important: If federal reclassification or descheduling of cannabis occurs, it could dramatically reshape the insurance landscape by opening the market to major national carriers. This would likely increase competition and drive premiums down. Stay informed on federal legislative developments, as they could directly impact your coverage options and costs.

How to Choose the Right Cannabis Insurance Broker

Not every insurance broker can effectively serve the cannabis industry. The unique regulatory environment, limited carrier market, and specialized risk profile of cannabis operations require a broker with specific expertise and relationships. When evaluating brokers, look for direct experience placing cannabis policies in New York, established relationships with multiple cannabis-friendly carriers, familiarity with OCM licensing and compliance requirements, and a willingness to review and adjust your coverage as your operation grows and regulations change.

Avoid brokers who treat cannabis insurance as an afterthought or who try to fit your operation into a standard commercial insurance template. The exclusions and coverage gaps that can hide in a poorly structured cannabis policy will only become apparent when you file a claim, and by then it is too late.

How Starisks Helps New York Cannabis Businesses Get Covered

At Starisks, we understand that cannabis operators face insurance challenges that most businesses never encounter. The limited carrier market, complex regulatory requirements, and elevated risk profile of the industry demand a broker who knows how to navigate this space and advocate for their clients.

We work with cannabis-friendly carriers and surplus lines markets to build coverage programs tailored to your specific license type and operation. Whether you are a cultivator protecting a grow facility, a processor managing extraction risk, a dispensary securing your inventory and premises, or a distributor covering your fleet, we put together a policy package that meets OCM requirements, satisfies your landlord and investors, and actually protects your business when something goes wrong.

Our approach starts with understanding your operation in detail: your license type, your facility, your revenue, your employee count, your supply chain relationships, and your growth plans. From there, we shop the market, compare options, and present you with clear recommendations. We also monitor regulatory changes and proactively reach out when your coverage needs to be adjusted, so you never fall out of compliance.

Get Cannabis Insurance That Actually Protects Your Operation

The cannabis insurance market is complicated, but finding the right coverage does not have to be. Book a free consultation with Starisks and let us build a coverage program designed for New York cannabis operators.

→ Schedule Your Free Cannabis Insurance Consultation