How to Protect Your Business from Losing Its Most Valuable Asset

Imagine this: your company’s lead developer, the one who built your entire platform from scratch, is suddenly gone. Or your founder, the person every investor and client relationship runs through, can no longer work. What happens to the business? For most small and mid-sized companies, the honest answer is that it would be a crisis. Key person insurance exists to prevent that crisis from becoming a catastrophe.

What Is Key Person Insurance?

Key person insurance is a life insurance or disability insurance policy that a business purchases on one or more of its most critical employees. The business owns the policy, pays the premiums, and is the beneficiary. If the insured person dies or, in some cases, becomes permanently disabled, the business receives the payout to help absorb the financial impact of losing that individual.

This is not a personal life insurance policy. The key person’s family does not receive the death benefit. Instead, the money goes directly to the business to cover the costs and disruptions that follow the loss of a critical team member.

What Does Key Person Insurance Cover?

The death benefit from a key person policy can be used for virtually any business purpose. The most common uses include covering revenue losses during the transition period, repaying business debts or lines of credit that the key person helped secure, funding the recruitment and training of a replacement, reassuring investors and lenders that the business can survive the loss, and buying out the deceased person’s ownership stake if they were a partner or shareholder.

Key Insight: Lenders and investors often require key person insurance as a condition of financing. If your business is seeking a loan or raising capital, having this coverage in place can strengthen your application and demonstrate financial preparedness.

Who Needs Key Person Insurance?

Not every employee qualifies as a key person. The question to ask is straightforward: if this person were suddenly gone, would the business face a significant financial hardship? If the answer is yes, that person is a candidate for key person coverage.

Startups with a Single Founder

In early-stage companies, the founder often is the business. They hold the vision, the client relationships, and in many cases the technical expertise that makes the product work. Losing a founder without key person insurance can mean the end of the company.

Partnerships and Co-Owned Businesses

When two or more people co-own a business, the death of one partner can create financial and legal complications. Key person insurance can fund a buy-sell agreement, providing the surviving partners with the cash to purchase the deceased partner’s ownership share from their estate without draining the business’s operating capital.

Businesses with Specialized Talent

If your company relies on a lead salesperson who generates a disproportionate share of revenue, a scientist holding critical patents, or a creative director whose vision defines the brand, these individuals represent concentrated risk. Key person insurance mitigates that risk by providing a financial buffer to find and onboard a replacement.

How Much Coverage Do You Need?

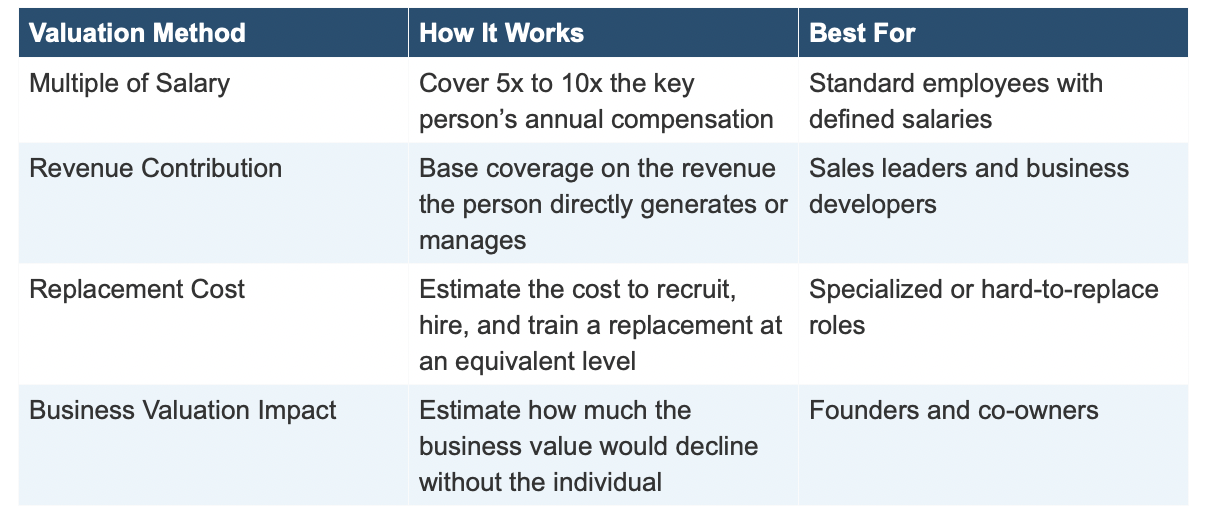

There is no single formula for calculating the right amount of key person coverage, but several widely used methods can help you arrive at a reasonable estimate.

valuation method table

Valuation MethodHow It WorksBest For Multiple of Salary Cover 5x to 10x the key person’s annual compensation Standard employees with defined salaries Revenue Contribution Base coverage on the revenue the person directly generates or manages Sales leaders and business developers Replacement Cost Estimate the cost to recruit, hire, and train a replacement at an equivalent level Specialized or hard-to-replace roles Business Valuation Impact Estimate how much the business value would decline without the individual Founders and co-owners

Most financial advisors recommend starting with a coverage amount that would sustain the business for at least two to three years while a transition is underway. Your broker can help you run scenarios based on your specific revenue, debts, and personnel structure.

Tax Considerations and Policy Structure

Understanding the tax implications of key person insurance is important for structuring the policy correctly. In general, the premiums the business pays for key person insurance are not tax-deductible. However, the death benefit the business receives is typically income-tax-free, which is a significant advantage.

The policy should be owned by the business entity, not by the individual or their family. The business pays the premiums and is listed as both the owner and the beneficiary. If the key person leaves the company, the business can cancel the policy, transfer ownership, or maintain it depending on the circumstances.

Important: Tax rules around life insurance can be complex, and there are specific IRS requirements that apply to employer-owned life insurance (EOLI) policies. Always consult a tax professional before purchasing key person coverage to ensure your policy is structured for compliance.

How Starisks Helps You Identify and Insure Key Person Risk

At Starisks, we help business owners assess their key person risk as part of a broader business insurance strategy. Many business owners know they have this vulnerability but are unsure how to quantify it or which type of policy to purchase.

We walk you through a structured risk assessment that identifies which individuals represent the greatest financial risk to the business, how much coverage is appropriate, and which policy type, term or permanent, makes the most sense for your situation. Because we work with multiple carriers, we can compare pricing and policy features to find the right balance between comprehensive coverage and affordable premiums.

Schedule a Key Person Risk Assessment

Do not wait for a crisis to find out your business is unprotected. Book a free risk assessment consultation with Starisks, and we will help you identify your key person vulnerabilities and build a coverage plan that keeps your business secure.