General Liability vs. Professional Liability Insurance: What New York Small Businesses Need to Know

If you own a small business in New York, you have probably been told you need liability insurance. But which kind? General liability and professional liability insurance protect your business from very different risks, and confusing the two, or skipping one entirely, can leave you dangerously exposed. This guide explains what each policy covers, how they differ, and when you need both.

What Is General Liability Insurance?

General liability insurance, sometimes called commercial general liability or CGL, is the foundational coverage that most businesses need. It protects you against claims of bodily injury, property damage, and advertising injury that arise from your business operations.

What General Liability Covers

If a customer slips on a wet floor in your office and breaks their wrist, general liability covers the medical expenses and any resulting lawsuit. If your employee accidentally damages a client’s property while performing work on-site, general liability pays for the repair or replacement. It also covers advertising injury, which includes claims like libel, slander, or copyright infringement in your marketing materials.

Who Needs General Liability?

Nearly every business that interacts with the public, operates from a physical location, or sends employees to client sites needs general liability insurance. In New York, many commercial landlords require tenants to carry a minimum amount of general liability coverage before signing a lease. If you are a contractor, retailer, restaurant owner, or service provider with a physical presence, this policy is non-negotiable.

What Is Professional Liability Insurance?

Professional liability insurance, commonly known as errors and omissions (E&O) insurance, protects your business against claims that your professional services or advice caused a client financial harm. Unlike general liability, which covers physical incidents, professional liability covers intellectual and service-based mistakes.

What Professional Liability Covers

If you are an accountant and a calculation error costs your client thousands of dollars in tax penalties, professional liability covers the claim. If you are a consultant and your strategic recommendation leads to a significant financial loss for a client, this policy protects you. It also covers claims of negligence, missed deadlines, failure to deliver promised services, and breaches of duty, even if the allegations are unfounded.

Industries That Commonly Need Professional Liability

Professional liability is essential for service-based businesses and licensed professionals. This includes accountants, architects, attorneys, consultants, engineers, financial advisors, healthcare providers, IT professionals, marketing agencies, and real estate agents. In New York, certain professions are legally required to carry professional liability coverage to maintain their licenses.

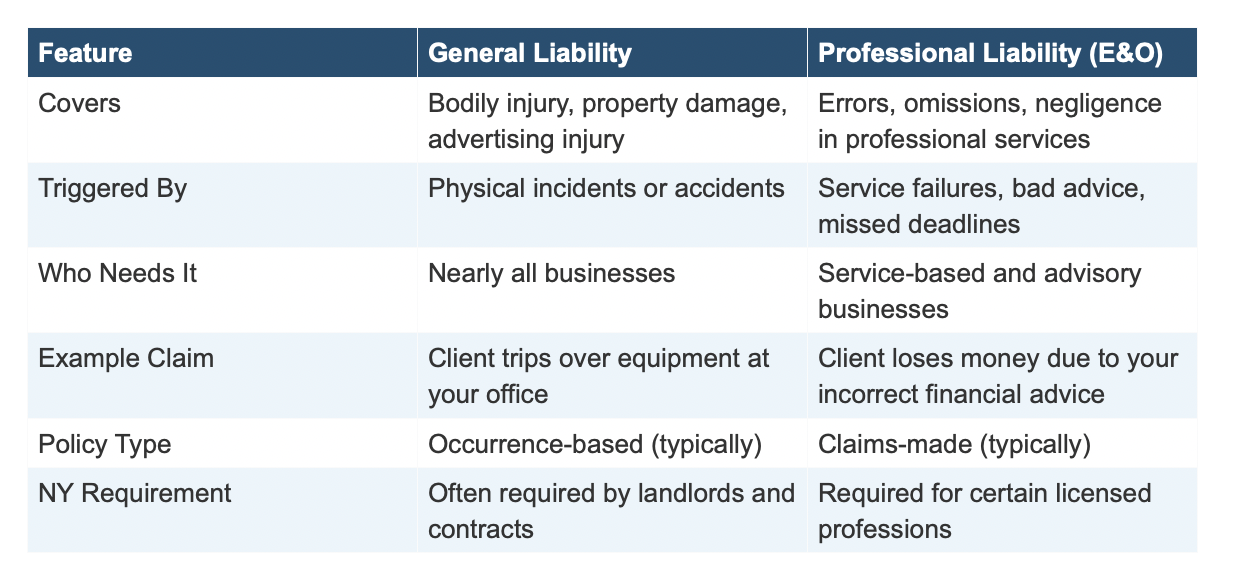

Key Differences at a Glance

general liability vs professional liability (E&O) table

New York-Specific Considerations

Operating a business in New York comes with specific insurance requirements and considerations that vary by industry and borough. Understanding these local factors is critical to ensuring you have the right coverage.

Contractors and Construction

New York State requires contractors to carry general liability insurance, and many project owners require minimum limits of $1 million per occurrence and $2 million aggregate. If you are working on public projects or in New York City, additional requirements may apply, including higher coverage limits and specific endorsements.

Consultants and Professional Services

Many corporate clients in New York require consultants to carry professional liability insurance before signing a contract. Common minimum requirements range from $1 million to $5 million, depending on the size and scope of the engagement. Technology firms, management consultants, and financial advisory firms are particularly likely to face these contractual requirements.

Healthcare Providers

Medical professionals in New York are required to carry medical malpractice insurance, which is a specialized form of professional liability. The minimum requirements vary by specialty, and premiums in New York tend to be among the highest in the nation. Healthcare providers also need general liability for their physical practice locations.

When You Need Both Policies

The short answer is that most service-based businesses in New York need both general liability and professional liability insurance. General liability covers the physical risks of running a business, while professional liability covers the intellectual and service-based risks. Having one without the other creates a gap that could be financially devastating.

For example, if you run an IT consulting firm, general liability covers a visitor who gets injured at your office, while professional liability covers a client who claims your software recommendation caused a data breach. Neither policy would cover the other’s scenario.

Cost-Saving Tip: Many insurers offer a Business Owner’s Policy (BOP) that bundles general liability with property insurance at a discount. You can then add professional liability as a separate policy or endorsement, depending on the carrier. An independent broker can help you find the most cost-effective combination.

How Starisks Helps New York Businesses Build the Right Coverage

At Starisks, we specialize in helping small businesses across New York build commercial insurance programs that actually match their risk profile. We do not sell one-size-fits-all packages. Instead, we start by understanding your business: your industry, your contracts, your client requirements, and your growth plans.

As an independent brokerage, we have access to multiple carriers and can compare coverage options, exclusions, and pricing to find the best fit. Whether you need standalone general liability, professional liability, or a comprehensive package that includes both, we build a coverage stack that protects your business without wasting money on unnecessary policies.

Get a Personalized Commercial Insurance Quote

Every New York business has unique risks. Let Starisks help you identify yours and build a commercial insurance program that provides real protection. Our consultations are free and come with zero obligation.