Term vs. Whole Life Insurance in 2026: Which Policy Is Right for Your Family?

Choosing between term and whole life insurance is one of the most important financial decisions your family will make. Both options provide a death benefit to protect your loved ones, but they work in fundamentally different ways, and the right choice depends on your financial goals, budget, and long-term plans. This guide breaks down everything you need to know so you can make a confident, informed decision.

What Is Term Life Insurance?

Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. If the policyholder passes away during that term, the insurer pays the death benefit to the named beneficiaries. Once the term expires, the coverage ends unless you renew it, usually at a significantly higher premium.

How Term Life Insurance Works

You select a coverage amount and a term length. In exchange, you pay a fixed monthly or annual premium for the duration of the term. The premiums are locked in and will not increase during the initial term period. If you outlive the policy, there is no payout, and the coverage simply ends.

Who Is Term Life Insurance Best For?

Term life is ideal for young families who need substantial coverage at an affordable price. It works well when your primary goal is to replace income during your working years, cover a mortgage, or fund your children’s education if something happens to you. It is also a strong choice for anyone who wants the most coverage per dollar spent.

Limitations to Consider

Term life does not build cash value. When the term ends, you have nothing to show for the premiums you paid. Renewing after the initial term can be extremely expensive, especially if your health has changed. If you need lifelong coverage, term life alone will not provide it.

What Is Whole Life Insurance?

Whole life insurance, also known as permanent life insurance, provides coverage for your entire lifetime as long as premiums are paid. It includes a cash value component that grows over time on a tax-deferred basis, functioning as both a protection tool and a savings vehicle.

How Whole Life Insurance Works

You pay a fixed premium, and a portion goes toward the death benefit while the rest accumulates as cash value. The cash value grows at a guaranteed rate set by the insurer. Over time, you can borrow against the cash value, withdraw from it, or use it to pay premiums. The death benefit is paid to your beneficiaries whenever you pass away, regardless of age.

Who Is Whole Life Insurance Best For?

Whole life makes sense for individuals who need permanent coverage, such as those with lifelong dependents, estate planning needs, or business succession strategies. It is also attractive to high-net-worth individuals who have already maximized other tax-advantaged accounts and want an additional vehicle for wealth accumulation.

The Cash Value Component

The cash value is one of the key differentiators. It grows at a guaranteed rate, and some policies pay dividends that can further increase the value. You can access this money during your lifetime through policy loans or withdrawals, which can serve as an emergency fund or supplement retirement income. However, outstanding loans reduce the death benefit.

Limitations to Consider

Whole life premiums are significantly higher than term premiums for the same death benefit amount. The cash value growth in early years is slow because a larger portion of your premium goes toward fees and insurance costs. Surrendering a whole life policy in the first several years typically results in a loss.

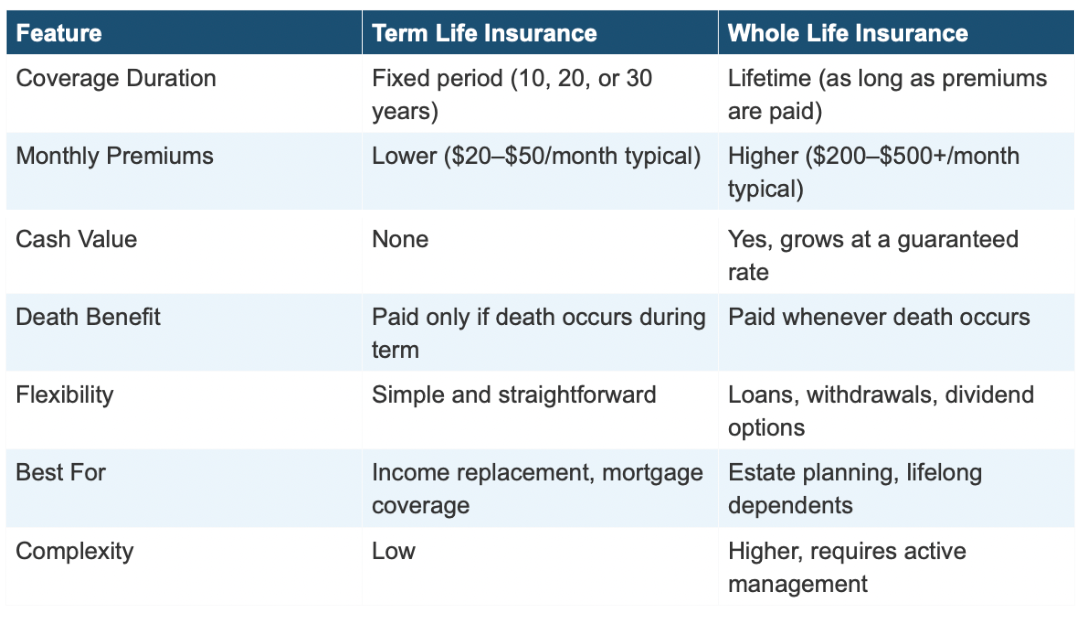

Side-by-Side Comparison: Term vs. Whole Life Insurance

Term vs. Whole Life Insurance Table Comparision

Which Policy Fits Your Situation?

Young Families on a Budget

If you are in your 20s or 30s, raising children, and working within a tight budget, term life insurance is almost always the better starting point. A 20- or 30-year term policy can provide $500,000 or more in coverage for a fraction of what a whole life policy would cost. This ensures your family is protected during the years when they depend on your income the most.

Business Owners and Entrepreneurs

Business owners often benefit from a combination of both. A term policy can cover business debts and buy-sell agreements, while a whole life policy can fund a succession plan or serve as collateral for business loans. Key person insurance, which protects the business if a critical team member passes away, is another important consideration for business owners.

High-Net-Worth Individuals and Estate Planning

If your estate is large enough to be subject to federal or state estate taxes, whole life insurance can play a critical role. The death benefit can provide liquidity to pay estate taxes without forcing your heirs to sell assets. When structured inside an irrevocable life insurance trust, the proceeds may be excluded from your taxable estate entirely.

The Hybrid Approach

Many financial advisors and insurance professionals recommend a blended strategy: purchase a large term policy for immediate, high-coverage needs, and layer on a smaller whole life policy for permanent coverage and cash value accumulation. This gives you the best of both worlds without overextending your budget.

Pro Tip: The “buy term and invest the difference” strategy only works if you actually invest the difference. If you lack the discipline to consistently invest the premium savings, whole life’s forced savings component may work better for you.

How a Broker Helps You Choose the Right Policy

Navigating life insurance options on your own can be overwhelming. An independent insurance broker like Starisks works differently from a captive agent who represents only one company. We shop across dozens of carriers to find the policy that fits your specific situation, whether that means a straightforward term policy, a whole life plan, or a combination of both.

At Starisks, we start every client relationship with a comprehensive needs analysis. We look at your income, debts, dependents, goals, and existing coverage to recommend a strategy that makes financial sense for your family. There is no one-size-fits-all answer, and the right policy for you today might look different five years from now. That is why we provide ongoing policy reviews to ensure your coverage keeps pace with your life.

Ready to Find the Right Life Insurance Policy for Your Family?

Book a free consultation with the Starisks team. We will walk you through your options, compare quotes from top-rated carriers, and help you build a coverage plan that gives your family real peace of mind.