How to Choose an Insurance Broker vs. Going Direct: What Nobody Tells You About Buying Insurance

Most people buying insurance face a choice they do not even realize they have. You can purchase coverage directly from an insurance company or through a captive agent who represents one carrier. Or you can work with an independent insurance broker who shops the entire market on your behalf. The difference might not seem significant, but it can dramatically affect the coverage you get, the price you pay, and the support you receive when you need it most.

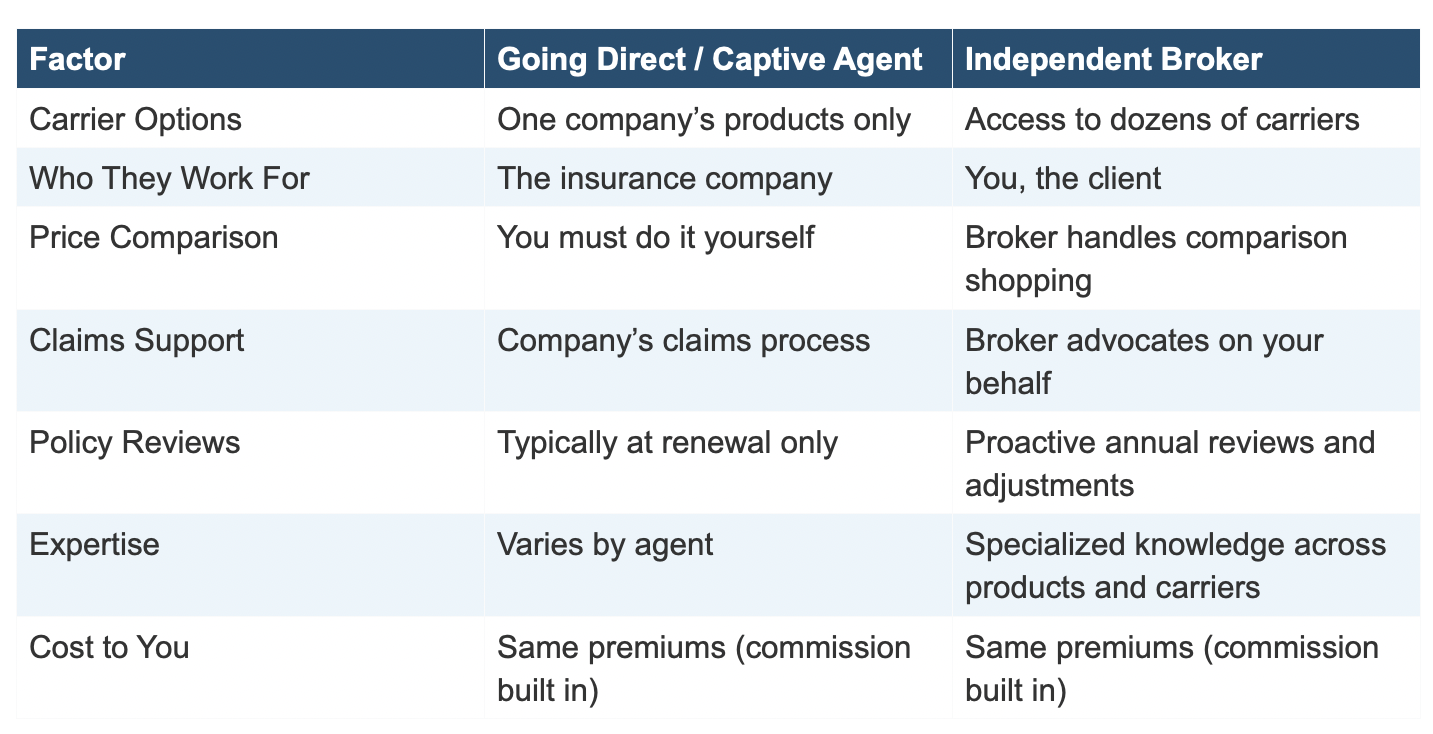

How Buying Insurance Directly Works

When you buy insurance directly, you are purchasing from a single company. This could mean going to a carrier’s website and filling out an application, or it could mean working with a captive agent who is employed by or exclusively contracted with one insurer.

Direct channels and captive agents can only offer you products from their own company. They may have excellent options within their portfolio, but they cannot show you what competitors are offering. If another carrier has a better rate for your risk profile, a more favorable policy structure, or fewer exclusions, you will never know unless you do the research yourself.

How Working with an Independent Broker Works

An independent insurance broker is not tied to any single carrier. Instead, a broker has relationships with dozens of insurance companies and can shop your coverage across the entire market. The broker works for you, not for the insurer.

When you work with a broker, they start by understanding your needs, your risk profile, and your budget. They then obtain quotes from multiple carriers, compare the coverage terms and exclusions, and present you with options along with their professional recommendation. Once you select a policy, the broker handles the application, coordinates with the carrier, and serves as your ongoing point of contact for questions, changes, and claims.

What You Lose When You Go Direct

The convenience of buying insurance online or through a single agent comes with trade-offs that most consumers do not fully appreciate until they need their coverage to work for them.

Limited Comparison

Without a broker, you are responsible for comparing policies across carriers on your own. This means reading through policy documents, understanding exclusions, and comparing coverage limits, all of which require expertise that most people do not have. Many direct buyers end up choosing based on price alone, which often means they are underinsured or carrying a policy with exclusions that would leave them exposed in a real claim scenario.

No Negotiation Leverage

Brokers have relationships with underwriters and volume leverage that individual buyers do not. They can often negotiate better rates, secure preferred underwriting, or request exceptions to standard terms that you would not be able to obtain on your own.

No Ongoing Policy Management

Your insurance needs change over time. You get married, buy a house, start a business, or have children. A captive agent may send you a renewal notice, but an independent broker proactively reviews your coverage annually and recommends adjustments as your life evolves.

The Broker Advantage

The Broker Advantage

Common Myths About Insurance Brokers

Myth: Brokers Cost More

This is the most persistent misconception, and it is simply not true. Brokers are compensated through commissions paid by the insurance carrier, not by you. The premium you pay is the same whether you buy through a broker or directly. In fact, because brokers can shop the market, they often find you a lower rate than you would find on your own.

Myth: Brokers Only Serve Wealthy Clients

While some brokerages focus on high-net-worth individuals or large commercial accounts, many independent brokers, including Starisks, work with individuals and small businesses at every income level. A good broker believes that personalized guidance should not be reserved for the wealthy.

Myth: Buying Online Is Faster and Easier

Online tools are great for getting a quick quote, but speed should not come at the expense of accuracy. Many online applications oversimplify the underwriting process, which can result in misclassification, missing discounts, or coverage gaps. A broker can often get you a policy just as quickly while ensuring the coverage actually matches your needs.

What to Look for in a Great Insurance Broker

Not all brokers are created equal. When evaluating potential brokers, look for proper licensing and credentials, including any specialized designations relevant to your insurance needs. Ask about their carrier relationships to understand how many options they can offer you. Pay attention to responsiveness, because how quickly and thoroughly a broker communicates before you are a client is a strong indicator of the service you will receive after.

Look for specialization. If you need commercial insurance, work with a broker who understands your industry. If you need life insurance, find someone who regularly works with the types of policies you are considering. A generalist may be fine for simple needs, but complex insurance requirements demand focused expertise.

How Starisks Operates as Your Independent Broker

At Starisks, our approach is built around a simple principle: we are on your side. Founded by Joel Goldman, Starisks operates as a fully independent brokerage, which means we are not obligated to recommend any specific carrier or product. Our only obligation is to find the best coverage for your situation at the most competitive price.

We start every relationship with a free, no-pressure risk assessment. We take the time to understand your full picture, your personal and financial goals, your business if applicable, and any existing coverage you have in place. From there, we shop the market, present clear options with honest recommendations, and handle the entire process from application to policy delivery.

Our commitment does not end when the policy is signed. We conduct regular reviews, help you adjust coverage as your life changes, and serve as your advocate if you ever need to file a claim. That is what our tagline means: Beyond a Policy. A Commitment to Care.

Experience the Broker Difference

Book a free 30-minute risk assessment call with the Starisks team. We will review your current coverage, identify any gaps, and show you what better protection looks like when you have an independent broker in your corner.

→ Schedule Your Free 30-Minute Call